Home Loan Guide for First-Time Buyers in Mumbai 2026: Eligibility, Interest Rates, PMAY Subsidy & Step-by-Step Process

Buying your first home in Mumbai is one of the most significant financial decisions you will ever make - and the home loan you choose will shape your finances for the next 20 to 30 years. In 2026, first-time buyers have never had it better: the RBI has cut the repo rate by a cumulative 125 basis points since early 2025, bringing it to 5.25%, home loan interest rates are at multi-year lows starting at 7.15% per annum, and the PMAY 2.0 subsidy scheme offers up to ₹2.67 lakh in upfront interest relief. Yet navigating banks, eligibility norms, documentation, and government schemes remains overwhelming for most buyers.

This guide walks you through every step - from understanding what lenders look at, to which bank offers the best rate, to how to claim your PMAY subsidy, to the exact stack of documents you need to carry on Day One.

What Banks Actually Look For: Home Loan Eligibility in Mumbai 2026

Lenders in Mumbai evaluate home loan applications across five key dimensions. Understanding each one before you apply will save you from surprises and rejection letters.

1. Age

The minimum age for a home loan applicant is 21 years. The maximum age at the time of loan maturity - not at application - is 65–70 years depending on the lender. This matters because it caps your tenure. A 45-year-old applicant will be offered a maximum 20–25 year tenure, not 30, which means higher EMIs.

2. Income and Employment Type

Banks in Mumbai accept the following income profiles:

|

Applicant

Type |

Min.

Monthly Income |

Stability

Requirement |

|

Salaried – Private |

₹25,000/month (net) |

2–3 years with current employer |

|

Salaried – Govt / PSU |

₹15,000/month (net) |

1 year with current employer |

|

Self-Employed Professional |

₹3–4 lakh/year net profit |

3 years ITR continuity |

|

Self-Employed Non-Professional |

₹4–5 lakh/year net profit |

3 years ITR + business continuity |

|

NRI / PIO |

Foreign income equivalent |

Foreign income docs required |

For joint applicants - co-borrowing with a spouse or parent - both incomes are clubbed, significantly increasing your loan eligibility.

3. CIBIL Score

This is non-negotiable. A CIBIL score of 750 or above is required to qualify for a home loan from most banks in Mumbai. A score between 700 and 749 may still get you a loan, but at a higher interest rate - often 0.25–0.50% more. Below 700, most lenders will decline.

4. Loan-to-Value (LTV) Ratio

Banks in India follow RBI-mandated LTV limits:

Property Value | Maximum Loan (LTV) |

Up to ₹30 lakh | Up to 90% |

₹30 lakh – ₹75 lakh | Up to 80% |

| Above ₹75 lakh | Up to 75% |

This means for a ₹1 crore flat in Mumbai - the most common price bracket for a 2BHK in the western suburbs - you need a minimum down payment of ₹25 lakh, with the bank funding ₹75 lakh.

5. The Fixed Obligation to Income Ratio (FOIR)

FOIR is the single most important number in your loan eligibility calculation. Most banks cap total EMI obligations at 40–50% of your net monthly income. If you earn ₹1 lakh per month and already have a car loan EMI of ₹12,000, the bank will calculate your remaining FOIR capacity at ₹38,000–₹50,000. The higher your existing obligations, the lower your home loan eligibility.

Rule of thumb: Pay off or close small loans (personal loans, car loans) before applying for a home loan. This maximises your eligible amount.

Current Home Loan Interest Rates in Mumbai - May 2026

The RBI held the repo rate at 5.25% in April 2026, maintaining the benefits of its 125 bps cumulative cuts since February 2025. Here is what Mumbai's leading banks and HFCs are offering as of May 2026:

|

Lender |

Rate

(p.a.) |

Max

Tenure |

Max

Loan |

|

SBI |

7.15%–8.05% |

30 years |

₹10 crore |

|

HDFC Bank |

7.75%–8.50% |

30 years |

₹15 crore |

|

ICICI Bank |

7.90%–8.65% |

30 years |

₹10 crore |

|

Axis Bank |

8.75%–9.50% |

30 years |

₹5 crore |

|

LIC HFL |

7.50%–8.75% |

30 years |

No upper limit |

|

Kotak Mahindra |

7.99%–9.25% |

20 years |

₹5 crore |

|

PNB |

7.20%–8.50% |

30 years |

₹10 crore |

|

Federal Bank |

8.15%–9.00% |

30 years |

₹5 crore |

Rates are floating (linked to repo rate or MCLR) and subject to lender revision. Always confirm current rates directly with the bank before signing.

How Much Has the Rate Cut Saved You?

A cumulative 125 bps cut translates into real rupee savings. Here is the impact on a standard Mumbai home loan:

|

Loan Amount |

Tenure | Monthly EMI Saving | Total Interest Saving |

| ₹30 lakh | 20 years | ~₹1,830 | ~₹4.39 lakh |

| ₹50 lakh | 20 years | ~₹3,050 | ~₹7.34 lakh |

| ₹75 lakh | 20 years | ~₹5,800 | ~₹13.94 lakh |

| ₹1 crore | 20 years | ~₹7,700 | ~₹18.5 lakh |

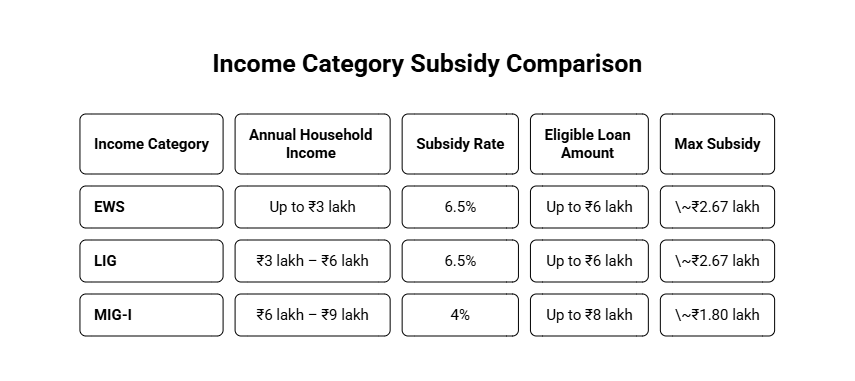

PMAY 2.0 Subsidy: How First-Time Buyers Can Save Up to ₹2.67 Lakh

The Pradhan Mantri Awas Yojana Urban 2.0 (PMAY-U 2.0) Interest Subsidy Scheme is one of the most valuable - and most underused - benefits available to first-time home buyers in India. Here is how it works in 2026.

Am I Eligible for PMAY 2.0?

You qualify if:

1. You or any family member does not own a pucca house anywhere in India

2. You have not received benefits under any Central, State, or Local Government housing scheme in the past 20 years

3. Your annual household income falls within the eligible categories

PMAY 2.0 Income Groups and Subsidy Structure

Under PMAY-U 2.0 Interest Subsidy Scheme, the ₹1.80 lakh benefit is disbursed in 5 equal annual installments of ₹36,000 each.

How to Claim the PMAY Subsidy - Step by Step

- Identify your income category - EWS, LIG, or MIG-I

- Apply for a home loan from an authorised PMAY lender - all nationalised banks, most private banks, and approved HFCs like LIC HFL, HDFC, PNB Housing qualify

- Declare your intent at loan application stage - ask the bank specifically for PMAY-CLSS benefit

- Fill the PMAY declaration form with household income details and self-certify that no family member owns a pucca house

- Bank verifies eligibility and forwards to the Central Nodal Agency (NHB or HUDCO)

- Subsidy is credited to your loan account, reducing your outstanding principal from Day One

Step-by-Step: How to Apply for a Home Loan in Mumbai

Step 1 - Establish Your Budget Before You Search

Before falling in love with any property, calculate your loan eligibility with precision:

- EMI rule: Your total monthly EMI obligations should not exceed 40–45% of your net take-home salary

- Down payment: Budget 25–30% of the property value as your own contribution (includes LTV gap + stamp duty + registration + move-in costs)

- Hidden costs to budget for: Stamp duty 5–6% (5% if property registered in woman's name), registration 1%, GST 1% (ready-to-move resale exempt), society deposit, interior work

Example: For a ₹80 lakh flat in Chembur, your total out-of-pocket expenses are approximately:

- Down payment (20%): ₹16 lakh

- Stamp duty (5%): ₹4 lakh

- Registration (1%): ₹80,000

- Interior + move-in: ₹3–5 lakh

- Total own funds needed: ₹24–26 lakh minimum

Step 2 - Get Your Documents Ready

Having your documents organised before approaching any bank speeds up approval significantly. You will need:

Identity & Address Proof

- Aadhaar Card

- PAN Card

- Passport (if available)

- Voter ID / Driving Licence

Income Proof (Salaried)

- Last 3 months' salary slips

- Last 2 years' Form 16

- Last 6 months' bank statements (salary account)

- Employment offer letter / appointment letter

Income Proof (Self-Employed)

- Last 3 years' ITR with computation sheet

- Last 3 years' audited P&L and Balance Sheet

- Business registration certificates / GST registration

- Last 12 months' business bank statements

Property Documents (once shortlisted)

- Sale agreement / allotment letter

- Title deed and chain of documents

- Approved building plan

- OC / CC from local authority

- NOC from society (for resale flats)

- MahaRERA registration certificate

Step 3 - Compare Lenders Beyond Just the Interest Rate

The interest rate is important, but do not stop there. Compare:

- Processing fees: Typically 0.25%–1% of loan amount (negotiable with good CIBIL)

- Prepayment / foreclosure charges: Floating rate loans have nil prepayment charges as per RBI rules, but confirm

- Loan disbursal timeline: Critical for under-construction properties with builder payment milestones

- Branch presence in Mumbai: For salaried, your loan servicing bank should have strong Mumbai presence

Step 4 - Apply, Respond Promptly to Queries, and Track Sanction

After submitting documents, the bank will:

- Conduct a technical valuation of the property

- Conduct a legal opinion on title documents

- Verify your employment and income

- Sanction the loan and issue a sanction letter (valid for 3–6 months)

Respond to every bank query within 24–48 hours. Delays on your end are the single biggest reason for loan processing taking 3–4 weeks instead of 7–10 days.

Step 5 - Registration, Disbursement, and Handover

- Register the sale deed at the local Sub-Registrar office with both buyer and seller present

- Bank disburses funds directly to the seller / builder on registration completion

- Obtain possession and keys

- Ensure society share certificate / index 2 is issued in your name

Common Mistakes First-Time Buyers Make with Home Loans in Mumbai

- Mistake 1 - Not checking CIBIL before applying: A surprise low score leads to rejection, which further dents your CIBIL. Check your score at least 6 months before your planned purchase.

- Mistake 2 - Borrowing the maximum the bank offers: Banks approve the maximum you are eligible for, not the maximum you should borrow. Cap your loan at a level where the EMI is comfortably within 35–40% of take-home pay, leaving room for life expenses and emergencies.

- Mistake 3 - Ignoring the total cost of ownership: The EMI is just one cost. Stamp duty, registration, GST, interior work, and society charges can add 15–20% to your all-in cost. Budget for all of them.

- Mistake 4 - Choosing a builder who does not have MahaRERA registration: Never pay any advance on a Mumbai property that lacks a valid MahaRERA registration number. Verify at rera.maharashtra.gov.in before signing anything.

- Mistake 5 - Not comparing at least 3–4 lenders: A difference of 0.25% over 20 years on a ₹75 lakh loan is approximately ₹2.5 lakh in total interest. It is worth spending 2 hours comparing lenders.

Best Areas for First-Time Home Buyers in Mumbai 2026: Price vs. Connectivity

If you are shopping for a ₹50–80 lakh budget, here are the most viable micro-markets in Mumbai's MMR in 2026:

|

Locality |

1BHK

Avg |

2BHK

Avg |

Metro

Access |

Verdict |

|

Chembur |

₹60–70L |

₹90L–1.1Cr |

Metro 2B, Monorail |

Strong livability |

|

Ghatkopar |

₹55–65L |

₹80–95L |

Metro Line 1 |

High rental demand |

|

Ulwe (Navi Mumbai) |

₹35–45L |

₹55–70L |

NMIA proximity |

Best cap. appreciation |

|

Kharghar |

₹40–55L |

₹65–80L |

NMIA + rail |

Established infra |

|

Virar-Vasai |

₹20–30L |

₹35–50L |

Western Railway |

Lowest entry point |

|

Dombivli |

₹35–45L |

₹55–70L |

Central Railway |

Strong micro-market |

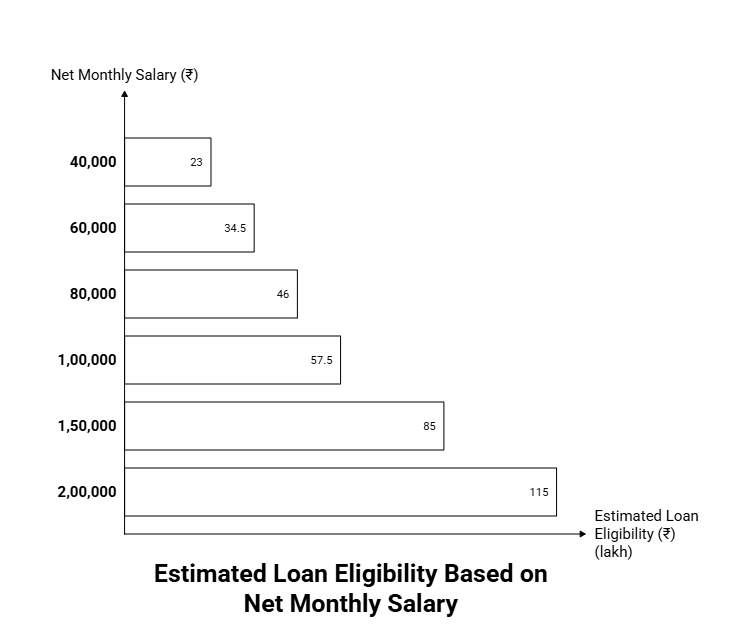

How Much Home Loan Can I Get in Mumbai? - Quick Eligibility Calculator

Use this quick formula as a starting point (actual eligibility depends on CIBIL, existing EMIs, and lender-specific norms):

- Net Monthly Salary × 50 × 55 ≈ Maximum Loan Eligibility

- (Assumes 50% FOIR cap, 55x multiplier for 20-year tenure)

For joint applications, add both incomes to arrive at combined eligibility.

Your First Home in Mumbai: The Action Checklist

Before you do anything else, run through this checklist:

- Pull your CIBIL score - target 750+ before applying

- Calculate your budget: income × FOIR – existing EMIs

- Save for down payment: 25–30% of target property value

- Shortlist your area based on budget and commute needs

- Check MahaRERA registration of any property you like

- Compare at least 3–4 lenders on interest rate + processing fees

- Check PMAY 2.0 eligibility if household income is below ₹9 lakh/year

- Engage a qualified property lawyer for title due diligence

- Do not pay any advance before loan sanction is in hand

Ready to Find Your First Home in Mumbai?

Buying your first home in Mumbai is a journey - and getting the home loan right is the most critical step. With interest rates at near-decade lows, PMAY subsidies on the table, and Mumbai's infrastructure network rapidly improving, 2026 is one of the best years to make that move.

Explore verified, RERA-registered properties across Mumbai and Navi Mumbai on blox.xyz - India's most transparent home buying platform. Use our home loan calculator, compare properties by EMI affordability, and connect with zero-brokerage experts who will guide you from shortlisting to keys.

Get in Touch

Let our experts help you answer your questions

Get in Touch

Let our experts help you answer your questions