RERA Documents Checklist for Mumbai Home Buyers 2026: Every Paper You Need Before, During & After Purchase

Buying property in Mumbai is one of the most significant financial commitments most people will make in their lifetime, yet a surprising number of buyers still approach the documentation process without a clear map. The result is last-minute scrambles, delayed registrations, loan rejections, and in the worst cases — fraudulent transactions that go undetected until it is too late.

This guide gives you a complete, stage-by-stage document checklist for buying property in Mumbai in 2026, with specific guidance on MahaRERA verification, NOC requirements, stamp duty calculations, and the regulatory updates that changed the game in January 2026. Whether you are buying a new apartment from a builder or a resale flat from an individual seller, every document category you need is covered here.

Why Documentation Is More Critical Than Ever in 2026

Two regulatory developments in 2025–26 have raised the documentation stakes for Mumbai property buyers:

1. Maharashtra's ₹1 Lakh Penalty for Insufficient Stamp Duty (effective January 2026) The state government now levies a minimum fine of ₹1 lakh for any transaction where stamp duty has been under-paid or incorrectly calculated. Previously, deficiency penalties were more modest and could be paid over time. The new penalty structure means even a genuine calculation error can cost buyers significantly. Getting your stamp duty right from the start is no longer just best practice — it is financial protection.

2. MahaRERA Mandatory Registration Expansion From 2026, MahaRERA has expanded mandatory registration requirements to cover projects over 500 sq metres OR more than 8 apartments — a lower threshold than the earlier rules. This means more developments are now legally required to be RERA-registered, and buyers of any project in this category must verify registration before making payments.

Understanding these changes, and having the right documents at every stage, puts you in control of one of the most important decisions of your life.

Stage 1: Pre-Purchase Due Diligence Documents

Before you sign anything or pay any booking amount, you need to gather and verify the following documents from the developer or seller.

1. MahaRERA Registration Certificate

What it is: Every new real estate project in Maharashtra must be registered on MahaRERA before it can be marketed or sold. The RERA registration number is the project's legal identity.

How to verify:

Go to maharera.mahaonline.gov.in

Search by project name, developer name, or RERA registration number

Check that registration status shows "Valid" (not expired or lapsed)

Verify the possession date matches what the developer has told you verbally

Check the complaint section — any active disputes or consumer complaints against the builder will appear here

Red flag: Any developer who does not share their RERA number or whose project does not appear on the MahaRERA portal should be treated as a serious concern. Do not pay any money to a project that cannot produce a valid RERA registration.

2. Title Deed / Mother Deed

What it is: The chain of ownership documents tracing the property back to its origin. For a new apartment, this means the developer's ownership or lease documents for the land. For a resale property, this means the complete transfer history from the original owner to the current seller.

What to look for:

Clear and unbroken chain of ownership

No missing links in the transfer history

Presence of all prior sale deeds, gift deeds, or inheritance documents

No conditional clauses that restrict resale or further transfer

This is the single most important document category. Engage a property lawyer to conduct a 30-year title search before purchase.

3. Encumbrance Certificate (EC)

What it is: An EC is a legal document certifying that the property is free of any monetary or legal obligations — unpaid mortgages, pending loans, or litigations. It is issued by the Sub-Registrar's office.

Why you need it: If a seller has an outstanding home loan from their bank, their lender has a charge on the property. Without an EC, you could unknowingly buy a property that the seller's bank still has a claim over. The EC reveals all such charges registered in the past 12–30 years.

Tip: Request an EC for a minimum period of 13 years. For very old properties, request 30 years.

4. Approved Building Plan

What it is: The structural and layout plan of the building as approved by the relevant municipal authority — MCGM (in Mumbai), NMMC (in Navi Mumbai), or MMRDA.

Why it matters: Construction that deviates from the approved plan is illegal. Unauthorised floors, added rooms, or structure modifications can make the building liable for demolition orders. Banks will not lend against unapproved construction.

What to check: Ensure the number of floors, unit layouts, and common areas in the approved plan match what is actually being built or what you are being sold.

5. Commencement Certificate (CC)

What it is: Issued by the municipal authority, the Commencement Certificate gives the developer permission to begin construction. A project without a CC is being built illegally.

Why it is non-negotiable: MahaRERA rules require the CC to be submitted at the time of project registration. If a developer cannot produce a CC, either the project is not RERA-registered or the RERA registration is fraudulent.

6. RERA-Registered Agreement for Sale Draft

What it is: Before any booking amount or advance is paid, you are legally entitled to receive the draft Agreement for Sale — the contract that governs your purchase. MahaRERA requires that this agreement be in a specified format.

What to check in the draft:

Exact carpet area measurement (not super built-up area)

Possession date with penalty clauses for delayed handover

Payment schedule linked to construction milestones

Specifications of materials to be used

Force majeure clauses and their scope

Refund and cancellation terms

Do not accept verbal assurances for anything that is not in the signed agreement.

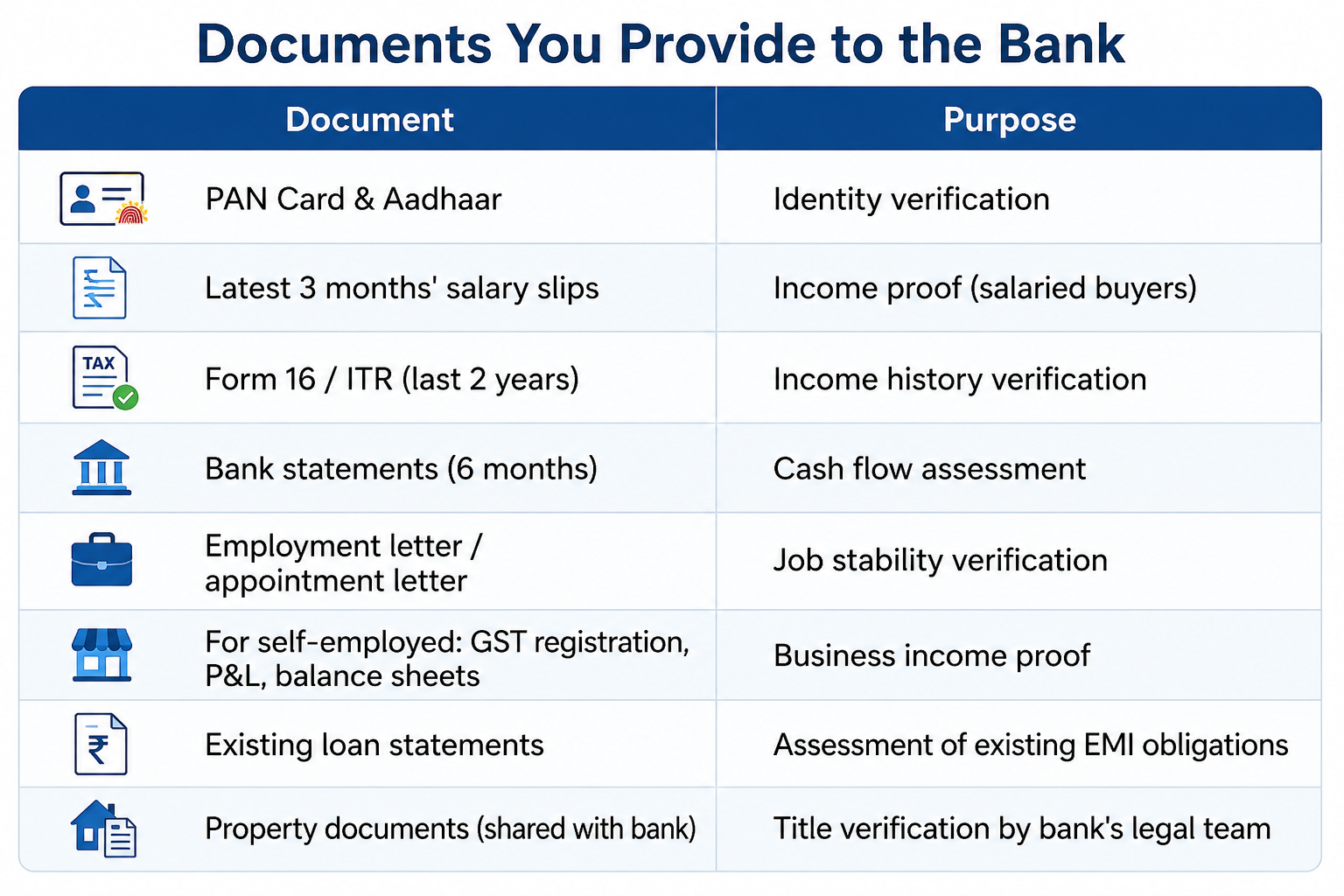

Stage 2: Home Loan Documentation

If you are financing your purchase with a home loan — which most Mumbai buyers do — you will need a parallel set of documents for your lender.

Documents You Receive from the Bank

Once the bank approves your loan, they issue the following — all of which are important for your purchase:

- Sanction Letter: The formal offer of a home loan, specifying the sanctioned amount, interest rate (fixed or floating), tenure, and conditions. Keep this document throughout your loan tenure.

- Disbursement Letter: Issued at each stage of disbursement for under-construction properties, or in one tranche for ready-to-move properties. This is the bank's confirmation of payment to the developer.

- Bank NOC (if existing security): If any collateral is involved or if the property previously had a mortgage, the bank issues a No Objection Certificate confirming it releases its claim before registration.

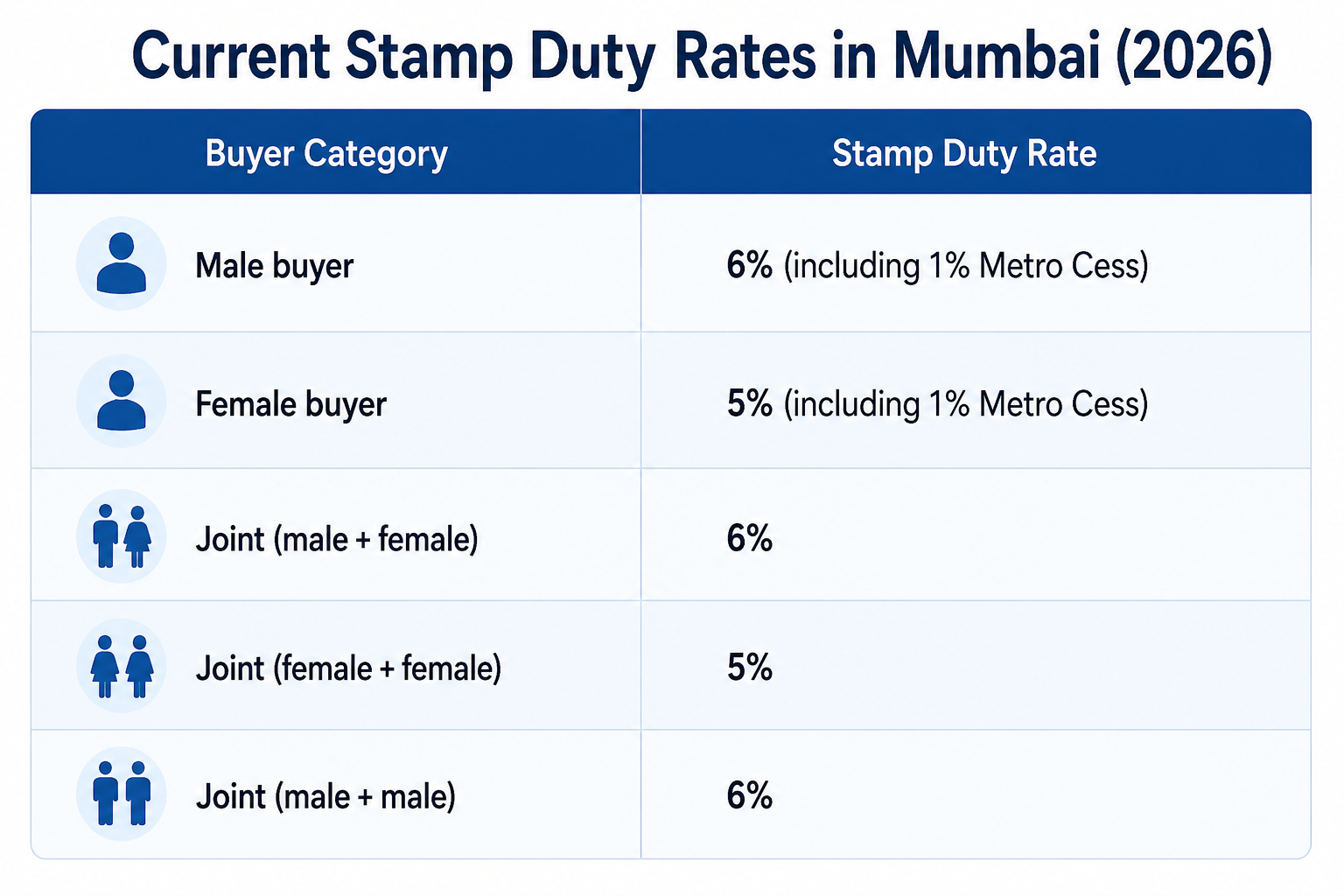

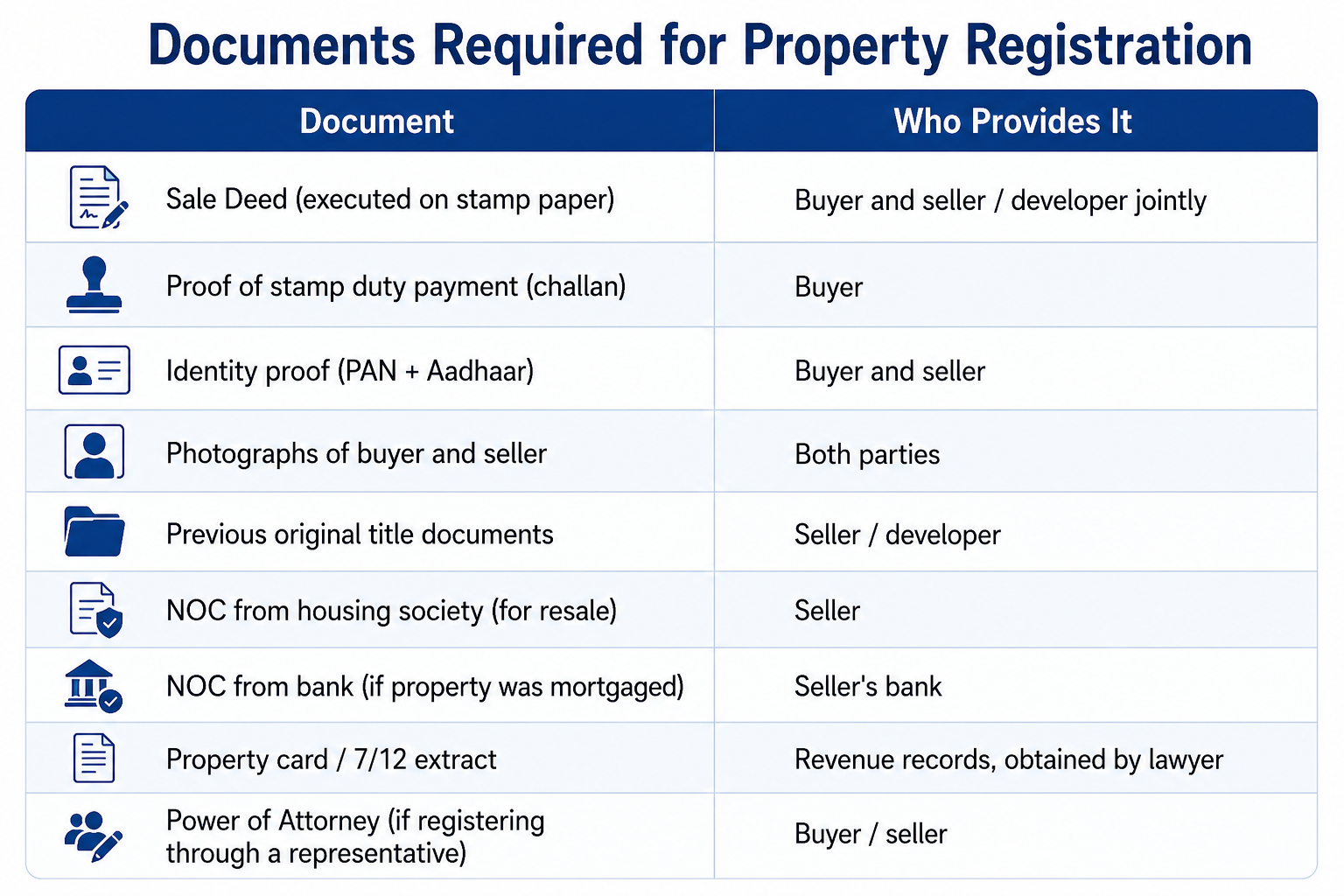

Stage 3: Stamp Duty and Registration Documents

This is the stage where the property officially changes ownership in the eyes of the law. Getting this stage right — particularly the stamp duty calculation — is essential given the January 2026 penalty changes.

Registration Charges: 1% of the property value, capped at ₹30,000 for properties above ₹30 lakh.

How Stamp Duty Is Calculated

Stamp duty is calculated on the higher of:

The actual sale price, OR

The Ready Reckoner (RR) rate — the government's floor value for properties in each locality

Example: If you purchase a flat in Bandra for ₹3 crore but the RR rate values it at ₹3.2 crore, stamp duty is calculated on ₹3.2 crore. Many buyers make the mistake of calculating on the sale price alone, which can now trigger the new ₹1 lakh penalty.

Tip: Always check the current Ready Reckoner rates for your locality at the IGR Maharashtra portal (igrmaharashtra.gov.in) before estimating your registration costs.

Stage 4: Society and Possession Documents

Once you take possession of the property, the documentation process enters its final phase: transferring membership to the housing society and ensuring all possession-related papers are in order.

Occupancy Certificate (OC)

What it is: Issued by NMMC, MCGM, or the relevant municipal authority, the OC certifies that the building has been completed as per the approved plan and is safe for occupation.

Why it is non-negotiable:

Banks will not release the final loan disbursement without an OC

A property without an OC is technically illegal to occupy

Electricity and water connections cannot be officially taken in a building without OC

Resale of a flat without OC is extremely difficult and undervalued

Always insist on taking possession only after the developer hands over a certified copy of the OC.

Completion Certificate (CC — Post-Construction)

Issued alongside or after the OC, the Completion Certificate confirms the building is structurally complete. Both OC and CC are required for full legal compliance.

Possession Letter

A formal letter from the developer to the buyer transferring possession of the specific unit. This document, along with the registered sale deed, is your primary ownership proof.

Share Certificate (for Cooperative Housing Societies)

Once the Cooperative Housing Society is formed (usually within 4 months of a sufficient number of flats being sold), each member receives a Share Certificate — a legal document establishing membership in the society. Keep this document safe; replacing a lost share certificate is time-consuming and expensive.

NOC from Housing Society (for Resale Properties)

If you are buying a resale flat from an existing member of a cooperative housing society, the society must issue an NOC confirming:

No outstanding maintenance dues

No pending society fees

Consent to the membership transfer

This NOC is required at the Sub-Registrar's Office at the time of registration and is a standard part of resale property transactions.

Stage 5: Post-Purchase Compliance Documents

Mutation / Property Tax Transfer

After registration, you need to update the property tax records in your name at the local municipal authority (MCGM or NMMC). This is called mutation. Without mutation, you may be unable to prove ownership for future sales or loans.

Documents needed for mutation:

Copy of registered sale deed

Copy of stamp duty receipt

ID proof of new owner

Completed mutation application form

Khata (for Navi Mumbai properties)

In NMMC jurisdiction (Navi Mumbai), the Khata is the municipal property register that records your ownership for tax purposes. Getting your Khata updated after purchase is mandatory for future property transactions.

Common Documentation Mistakes Mumbai Buyers Make

Mistake 1: Paying booking amounts before RERA verification Never pay anything — not even a token amount — before verifying the project's RERA registration number on the MahaRERA portal. Unregistered projects have no regulatory protection for buyers.

Mistake 2: Not insisting on carpet area in writing RERA mandates that all sales be on the basis of carpet area. If a developer quotes you in terms of super built-up area only, insist on the carpet area disclosure. A loading factor of 30–40% is not uncommon, and this directly impacts your per-sq-ft cost.

Mistake 3: Skipping the encumbrance certificate on resale Many resale buyers skip the EC because the seller seems trustworthy. A hidden mortgage charge on the property can result in you inheriting someone else's debt. Always get the EC.

Mistake 4: Under-declaring the property value In the past, some buyers under-declared property values at registration to save on stamp duty. The new ₹1 lakh minimum penalty for stamp duty deficiency and stricter IGR enforcement makes this practice extremely risky in 2026.

Mistake 5: Not reading the agreement for sale The Agreement for Sale is the most powerful document in your possession. Builders often include clauses that restrict your remedies for delays, alter promised specifications, or limit your rights in disputes. Every clause must be read and, where necessary, negotiated before signing.

Conclusion: Documentation Is Your Strongest Protection

The Mumbai property market in 2026 is large, dynamic, and largely well-regulated thanks to MahaRERA — but regulations only protect buyers who engage with them. A buyer who verifies RERA registration, reads the Agreement for Sale, checks the Encumbrance Certificate, and calculates stamp duty correctly is protected by one of the strongest property buyer frameworks in India. A buyer who skips these steps because a deal looks good or a developer seems reputable is taking on unnecessary risk.

Use this checklist as your starting point. Engage a qualified property lawyer for every transaction — the cost of legal advice is trivially small compared to the cost of a documentation error on a ₹1–2 crore property.

Get in Touch

Let our experts help you answer your questions

Get in Touch

Let our experts help you answer your questions