Under-Construction vs Ready-to-Move Property in Mumbai 2026: Which is the Better Investment?

Mumbai's property market never sleeps, and neither does the debate between buying an under-construction flat or a ready-to-move-in (RTM) home. Whether you're a first-time buyer hunting for the right entry point, or a seasoned investor looking to maximise ROI, this choice can mean a difference of ₹20–40 lakh or more over the life of your investment.

In 2026, both options carry distinct advantages and real risks. New infrastructure like the Navi Mumbai International Airport (NMIA), Mumbai Metro Line 3, and the Mumbai Trans Harbour Link (MTHL) have reshaped the appreciation map. GST rules, RERA protections, and shifting demand patterns have changed the calculus too. This guide breaks it all down, so you can make the call that's right for your goals and budget.

What Is Under-construction Property (and How Is It Different)?

Under-construction property or "UC" - refers to any flat, apartment, or villa that is sold before or during the construction phase. Buyers typically enter at the project-launch stage (or at a "pre-launch" even before RERA registration), with possession anywhere from 2 to 5 years away.

Ready-to-move (RTM) properties, by contrast, are completed units with an Occupation Certificate (OC) in hand. You can inspect the flat, verify the society, check actual floor finishes, and move in or start collecting rent, within weeks of registration.

The distinction matters enormously for taxes, financing, risk, and returns. Let's go through each factor in detail.

Price: Who Wins on Entry Cost?

In May 2026, data from Mumbai's primary market shows:

|

Property Type |

Average Price (₹/sqft) |

YoY Appreciation |

|

Under-Construction

(UC) |

₹32,900 |

+2.77% |

|

New Launch |

₹31,600 |

+4.44% |

|

Ready-to-Move

(OC Received) |

₹36,500–₹42,000 |

+6–8% |

Under-construction and new-launch properties are typically priced 10–25% lower than equivalent RTM units in the same micro-market. In premium corridors like Andheri West, Bandra, or Worli, that gap can translate to ₹30–50 lakh on a typical 2BHK. In emerging markets like Panvel, Dronagiri, or Kharghar, the gap tends to narrow but the appreciation upside is higher.

The catch: Lower sticker price doesn't mean lower total cost. Factor in GST.

GST: A Critical Difference in 2026

This is one of the most misunderstood aspects of the Under-construction vs. RTM debate.

|

Property Type |

GST Rate (2026) |

|

Under-construction

(above ₹45 lakh) |

5% (no ITC) |

|

Under-construction

(affordable, ≤₹45 lakh) |

1% |

|

Ready-to-move

(OC received) |

NIL (GST Exempt) |

On a ₹1 crore under-construction flat, you pay ₹5 lakh in GST. On a ₹1.5 crore flat, that's ₹7.5 lakh — an amount that almost entirely offsets the apparent discount you got over RTM.

For buyers in the affordable segment (sub-₹45 lakh), GST at 1% makes Under-construction significantly more attractive. But at mid-market and premium price points, the GST differential must be calculated carefully before assuming you're "getting a deal."

Practical tip: Always compare the all-in price (sticker + GST + registration + stamp duty) when evaluating Under-construction vs RTM.

Construction-Linked Plans vs Immediate EMIs: Cash Flow Comparison

One financial advantage of Under-construction that's often overlooked is payment flexibility. Most UC projects offer Construction-Linked Payment (CLP) plans - you pay in tranches tied to construction milestones (foundation, slab casting, floor completion, etc.).

This means:

- You don't pay the full amount upfront

- Your EMI burden grows gradually, not immediately

- You can invest surplus funds in other assets during the construction period

With RTM, you need the full mortgage from Day 1 — and your EMI clock starts immediately. If you're not going to use or rent the property right away, you're paying full EMI without any income offset.

Scenario: ₹1.2 crore property, 75% bank-financed at 8.75% for 20 years

|

|

Under-Construction (CLP) |

Ready-to-Move |

|

Month 1 EMI |

₹28,000 (on

first tranche) |

₹1,06,000 (full

loan) |

|

EMI at

possession (2 yrs) |

₹1,06,000 |

₹1,06,000 |

|

Carry cost

savings (2 yrs) |

~₹18–22 lakh |

— |

|

Rental income

start |

Post-possession |

Immediate |

For investors who plan to rent out, RTM wins on immediate cash flow. For buyers who need gradual payments, UC plans are kinder on monthly budgets.

Appreciation: Where Returns Are Actually Being Made in 2026

This is where the numbers get genuinely exciting — and where many buyers miss the real opportunity.

Infrastructure-driven appreciation zones: Mumbai's new infrastructure has created dramatic appreciation corridors that disproportionately favour Under-construction buyers who entered early.

|

Infrastructure Driver |

Appreciation Impact |

Key Micro-Markets |

|

NMIA (Navi

Mumbai Airport) |

Up to 23% price

surge |

Dronagiri, Ulwe,

Panvel |

|

Metro Line 3

(Aquamarline) |

8–18% faster |

BKC, Worli,

Dadar, Andheri E |

|

MTHL |

15–20% |

Nerul, Belapur, Pushpak

Nagar, Sewri |

|

Coastal Road |

10–12% |

Bandra, Worli |

Emerging areas like Panvel, Kharghar, and Ulwe have recorded 12–18% annual appreciation for under-construction units bought at pre-launch prices. Compare this to the 6–10% typical of saturated RTM markets in Andheri or Goregaon, and the case for early entry in growth corridors becomes clear.

Key insight: Under-construction in the right location — particularly infrastructure-linked zones — consistently outperforms RTM on capital appreciation. The trade-off is a longer wait and higher risk of delay.

Risk: The Real Downside of Under-Construction Property

Let's be direct. Under-construction property in Mumbai carries three risks that RTM buyers simply don't face.

1. Construction Delays:

Even with RERA protection, delays are common. A project slated for possession in December 2026 may not deliver until 2028. Each year of delay costs you:

- Lost rental income (₹3–8 lakh/year depending on the unit)

- Continued EMI outgo without occupancy

- Opportunity cost on funds locked in the project

2. Plan Deviations and Design Changes

Brochure renders and actual delivery don't always match. Amenities get downgraded. Specifications change. Layouts may be modified. While RERA mandates that changes affecting more than one-third of the originally approved plan need buyer consent, smaller deviations can still disappoint.

3. Developer Default or Project Stalling

While rare with established developers, project stalling is a real risk with smaller or less-capitalised builders. Before buying any UC project, verify:

- MahaRERA registration (mandatory — check at maharera.maharashtra.gov.in)

- Escrow account compliance: 70% of buyer funds must be deposited into a project-specific bank account, withdrawable only with certification from architect, engineer, and CA

- Developer's track record of past deliveries

In 2025 alone, MahaRERA disposed of nearly 7,000 complaints — demonstrating that the system is active, but also that disputes are frequent enough to warrant caution.

RERA's Buyer Protection Shield

Thankfully, RERA provides significant protection for UC buyers in Maharashtra:

- Structural defect liability: Developer is liable for 5 years post-possession

- Compensation: If delayed, buyer can claim interest on amounts paid

- Refund right: If you choose to exit, RERA entitles you to a refund with interest

- Transparent milestones: RERA-registered projects display construction progress on the public portal

The bottom line on risk: Choose RERA-registered projects only. Research the developer's completion history. Avoid projects from first-time developers or those with ongoing complaints on MahaRERA.

Rental Income: RTM Wins, But the Gap Is Closing

If immediate rental income is your goal, RTM wins — no question. You register the property, find a tenant, and start collecting rent.

With Under-construction, you wait for possession, then set up the flat (furnishing, minor works), find a tenant, and only then see cash flow. Depending on the project timeline, that's 2–4 years of zero rental income.

However, appreciation in under-construction units in high-growth zones means that by the time you take possession, the rental value has also climbed. A 2BHK in Dronagiri bought at ₹75 lakh under-construction in 2023 might today command ₹20,000–25,000/month in rent — while its current market value has risen to ₹95–1.05 crore.

Rental yields in Mumbai vary by location and configuration:

|

Area |

Rental Yield |

Best Config |

|

Andheri East |

3.2–3.8% |

1BHK, 2BHK |

|

Powai |

3.0–3.5% |

2BHK |

|

Goregaon |

3.0–4.0% |

1BHK |

|

Ghatkopar |

3.5–4.2% |

1BHK, 2BHK |

|

Kharghar (Navi

Mumbai) |

3.5–4.5% |

2BHK |

|

Bandra/Khar |

2.0–2.5% |

1BHK, studio |

|

Worli/Lower

Parel |

2.0–2.8% |

Premium 2BHK |

Verdict: For pure rental income, RTM is superior. For long-term appreciation + rental income combination, well-chosen UC in growth corridors can outperform over a 5–7 year horizon.

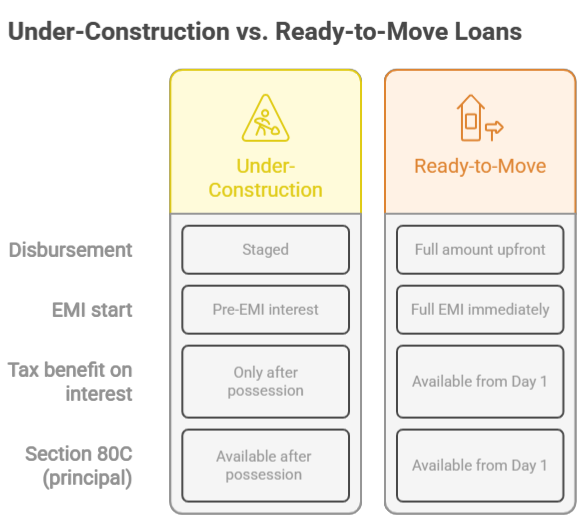

Home Loan and Financing: What Banks Prefer

Both under-construction and ready-to-move properties are eligible for home loans in Mumbai. But there are nuances:

The tax implications are significant. A buyer in the 30% tax bracket financing a ₹1.2 crore home is potentially looking at ₹2–3 lakh/year in deferred tax benefits if they buy under-construction vs RTM. Consult your CA to model the full tax impact before deciding.

Who Should Buy Under-construction in Mumbai?

Under-construction is a smart choice if:

- You have a flexible timeline and won't need the property for 3–5 years

- You're investing in an infrastructure-linked growth corridor (NMIA, Metro, MTHL zones)

- You want lower upfront capital commitment with CLP payment flexibility

- You're disciplined enough to evaluate developers by RERA track record

- You're targeting capital appreciation over immediate rental income

Who Should Buy Ready-to-Move in Mumbai?

RTM is the right call if:

- You need to move in (or start earning rent) within the next 6–12 months

- You want to avoid GST (saving 5% on mid-market homes)

- You want what-you-see-is-what-you-get certainty on quality, layout, and neighbourhood

- You're risk-averse or have experienced delays on prior projects

- You want immediate home loan tax benefits under Section 24 and 80C

Key Red Flags: What to Avoid in Either Category

In Under-Construction:

- Developers without a completed project track record

- Projects not registered on MahaRERA

- Possession dates more than 4 years away without a compelling growth story

- Escrow non-compliance (check RERA portal)

- Projects with more than one pending complaint per 100 sold units

In Ready-to-Move:

- Properties without a valid Occupation Certificate (OC)

- Societies with pending BMC notices or unauthorised construction

- Older buildings (20+ years) without recent structural audits

- Properties with unresolved title disputes or encumbrances

The Blox.xyz Verdict: Making the Call in 2026

There's no universal winner here — the right choice depends on your situation, timeline, and goals.

Buy Under-construction if you're an investor or end-user with time on your side, targeting the NMIA zone, Metro-3 corridor, or emerging Navi Mumbai pockets where the appreciation story is still unfolding. Enter with RERA-registered developers only, and factor in the true all-in cost including GST and carry charges.

Buy Ready-to-Move if you're a family buyer, need quick possession, want to avoid GST, or are looking for a stable rental-income property in an established neighbourhood.

Whichever direction you choose, data-backed decision-making — comparing real appreciation history, checking MahaRERA status, and modelling your actual holding period returns — is the single most important habit to develop as a Mumbai property buyer in 2026.

Ready to explore under-construction and ready-to-move listings across Mumbai and Navi Mumbai?** Browse verified RERA-registered projects and compare investment options on blox.xyz.

*This article is for informational purposes. Property investments involve risk. Consult a certified financial planner and legal advisor before making investment decisions.*

Get in Touch

Let our experts help you answer your questions

Get in Touch

Let our experts help you answer your questions