NRI Home Loan India 2026: Best Banks, Interest Rates, FEMA Rules & How to Apply from Abroad

Buying property in Mumbai from abroad is more achievable than most NRIs realise — but it requires understanding a financing and compliance framework that differs significantly from what a resident Indian buyer faces.

FEMA Rules: What NRIs Can Buy

NRIs can purchase residential apartments, houses, commercial property, and properties under construction from RERA-registered developers. Restricted (without RBI approval): agricultural land, plantation property, farmhouses. All Mumbai residential and commercial property falls within the permitted category.

All property payments must flow through an NRE or NRO account in INR. Foreign currency payments directly are not FEMA-compliant.

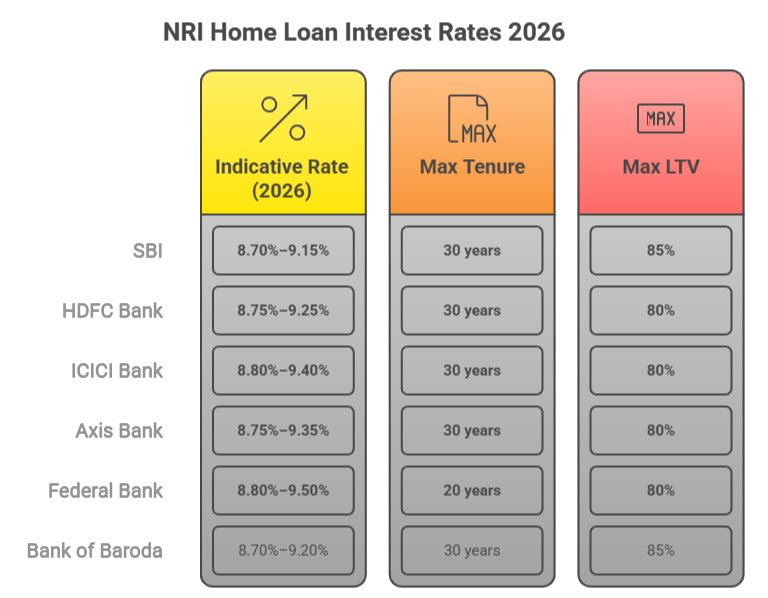

NRI Loan Eligibility Summary

Valid Indian passport + OCI/PIO status | 1–3 years continuous overseas employment | Age 21–60 | Active NRE/NRO account | Clean CIBIL history. Self-employed applicants need 3 years business vintage.

TDS Rules & 2026 Budget Update

Buying from NRI seller: TDS 12.5% on LTCG (held >2 years), 30% on STCG (held ≤2 years). Key 2026 change: From October 2026, TDS can be deposited using buyer's PAN instead of TAN — eliminating a 4–6 week procedural delay for NRI-to-NRI transactions.

Repatriation Requirements

File Form 15CA (self-declaration) and Form 15CB (CA certificate) before bank remittance. Cap: USD 1 million per financial year from NRO account. NRE funds: freely repatriable without annual cap.

Need help finding RERA-verified projects in Mumbai within your NRI home loan budget

Get in Touch

Let our experts help you answer your questions

Get in Touch

Let our experts help you answer your questions